9 Best Small Business Loans in 2023 [Compare Options]

Shawn Manaher

•

Updated on December 8, 2022

Small businesses need capital to get up and running. From buying equipment, renting a space, and paying employees, there are plenty of reasons you may be in search of a small business loan.

We’ve gathered the best small business loans, saving you the time and hassle of comparing multiple options yourself. You can focus your energy on running your business instead of shopping for loans. With any of the following small business loans, you can make large purchases or simply have enough cash flow to run your business. You must simply decide which of our top picks is right for your business.

Table of Contents

What Are The Best Small Business Loans In 2023?

The best small business loans will look different for every business. Some will do best with SBA loans, while others will find success with term loans or lines of credit. As you compare our top picks, consider the following:

The type of loan

Your credit score

Your business type or industry

The amount you need to borrow

Whether you want a lump sum or the funds as-needed

How long it takes to receive funding

The interest rate

Additional fees (including prepayment penalties)

How long you want the loan term to be

Requirements (including time in business, annual cash flow, and annual credit score)

Repayment flexibility, including penalties for prepayment

Customer support

Reputation of the lender

Your preference for online lenders, banks, and credit unions, or do you have no preference

If you decide that an SBA loan is right for you, consider getting it through the U.S. Small Business Administration. This is a unique option on the list because the SBA isn’t a lender; it connects you with authorized lenders. There is a convenient lender match tool to help you do that. It’s important to keep in mind that you need to use personal assets and alternative financial resources before you can apply for an SBA loan.

Highlights

You can choose from a line of credit or a term loan, including options with long repayment terms.

Choose from various types of loans, including 7(a), 504, and microloans.

Loans are available for anywhere from $500 to $5.5 million. Some loans will restrict how you can use the funds, but many don’t.

Loans can have terms of up to 25 years.

The interest rates are capped, so it should not be too expensive. The rates and fees are also usually very competitive.

You will likely need a personal guarantee as well as collateral, but you can find some loans that don’t require either.

Direct loans from the SBA are available if you are recovering from a disaster that has been declared.

SBA loans typically have flexible overhead requirements and lower down payments.

Some of the loans include continued support with running your business.

Pricing

Because you get matched with various lenders via the SBA, there is no set price range. You will be able to compare terms, fees, rates, and more between various lenders. That said, you can typically borrow up to $5,000,000, with an APR of 9.25 to 11.75%.

Interest rates for SBA 7(a) loans are 5.5% to 11.25%. Rates for SBA 504 loans are 2.81% to 4%. They are 8% to 13% for SBA microloans.

Bottom Line

If you have already tried other options and used your personal assets, then a loan from the Small Business Administration can be an appealing option. Because these loans come from a government agency, there are caps on the interest rates, and you can trust that the loans are legitimate. You also get to compare multiple loans from various approved lenders, giving you more options. The big caveat is that you must have exhausted all your other financing options before applying via the U.S. SBA. As such, not all businesses are eligible. If, however, you have exhausted your options, this can be a lifeline for your business. It is also worth noting that processing times for these loans can be longer than those for others on the list.

OnDeck is an appealing option for small businesses that want to apply for a loan and complete the entire process online. Note that interest rates are higher than for some others on this list. But with a maximum loan amount of $250,000 and a minimum credit score requirement of 625, they are still a popular and highly-rated option.

Highlights

Your credit score only has to be 625.

Loans can range from $5,000 to $250,000, and lines of credit can be $6,000 to $100,000. Repayment terms are up to 24 months and 12 months, respectively.

OnDeck has provided $14 billion of funding to businesses, giving you confidence in its reputation. It has an A+ BBB rating and a 4.8/5 rating on Trustpilot.

It is easy to apply with minimal paperwork, and you can receive your cash the same business day.

You will make repayments either daily or weekly, which is a different structure than most loans on this list. OnDeck reports your payments, building your business credit score.

Those who qualify for 100% Prepayment Benefits can pay in full early and not have to pay any remaining interest nor any fee or penalty.

You will need a personal guarantee and place a business lien.

Businesses operating for at least a year are eligible. You must not have had bankruptcies in the last two years and have a $100,000 minimum annual revenue.

Loans are not available to businesses in North Dakota, South Dakota, or Nevada.

Pricing

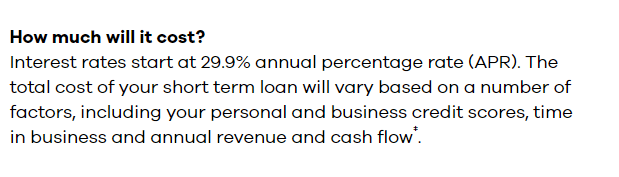

Short-term loans and lines of credit have interest rates starting at 29.9% APR. Your total loan cost depends on your personal credit score, business credit score, cash flow, annual revenue, and time in business. If you have less-than-stellar credit, your APR can be as high as 97.30%, so pay close attention to your offer details.

Bottom Line

Businesses in search of a short-term loan or a line of credit that need the funds as soon as possible will want to consider OnDeck. You can receive your funding the same business day and find the application process incredibly easy. You just need to be aware of the comparatively high-interest rates from this lender. For many businesses, however, the convenience of applying online and getting fast funding makes up for those high rates.

Fundbox is very popular for business owners who aren’t eligible for other options and want a line of credit. It requires only a minimum credit score of 600, so qualifying for a loan is much easier than with other lenders on this list. You can use the business line of credit to fill in gaps in your cash flow.

Highlights

The application process is simple, with a minimum credit score of 600. Applying doesn’t affect your credit score. You can get a decision within three minutes.

Your business needs only six months of history to apply, which is less than most other options. The minimum annual revenue is $100,000. You need a credit score of 600.

You can receive your financing within a business day, giving you access to funds quickly. Your revolving line of credit can be $1,000 to $150,000.

There are no account maintenance fees, inactivity fees, or prepayment penalties. You choose your repayment plan.

Using your Flex Account gives you an extra three business days to make repayments. There are no fees for payments with debit cards or ACH transfers.

These are short-term loans for up to 24 weeks, and you need to make weekly payments.

Fundbox Plus is coming soon, which will give you more time to pay and 20% lower fees.

Fundbox has helped more than 500,000 businesses by providing more than $3 billion working capital.

It has an A+ rating from the Better Business Bureau and a Trustpilot rating of 4.7/5 with more than 3,000 reviews.

The mobile app makes applying, accessing funds, making payments, and monitoring your line of credit incredibly easy.

Pricing

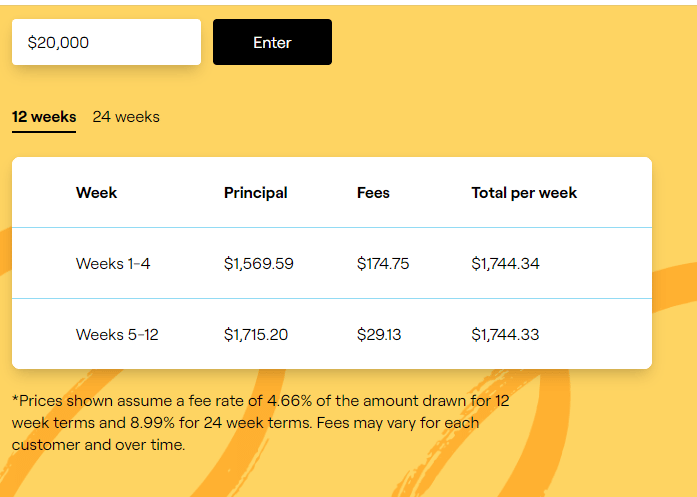

Your interest rate with Fundbox can be anywhere from about 10.10% to 79.80%. The website has a convenient line of credit calculator that lets you easily view how much you can expect to pay in fees. This calculator assumes 4.66% fees for 12-week terms and 8.99% fees for 24-week terms.

Bottom Line

Fundbox is a good option if you want a short-term line of credit of up to $150,000. It is much easier to qualify for a line of credit from Fundbox than many others on our list, as your credit score needs only to be 600 and your business in operation for at least six months. Most other options have stricter requirements. The application process is also fast, enabling you to get your funds the next business day. These factors make this small business loan option appealing to business owners.

Funding Circle is worth considering if you are an established business that needs funding to refinance debt or expand. The typical APR is between 10.64% and 31.85%, making it one of the more affordable options on the list. Keep in mind that there is a minimum credit score of 660. You can borrow up to $500,000 with a line of credit or $5 million with an SBA 7(a) loan.

Highlights

Funding Circle has an A+ BBB rating and has provided more than $19.4 billion of funding to 130,000 companies around the world.

Funding Circle works with 700 industries.

Use a single application to qualify for all three products.

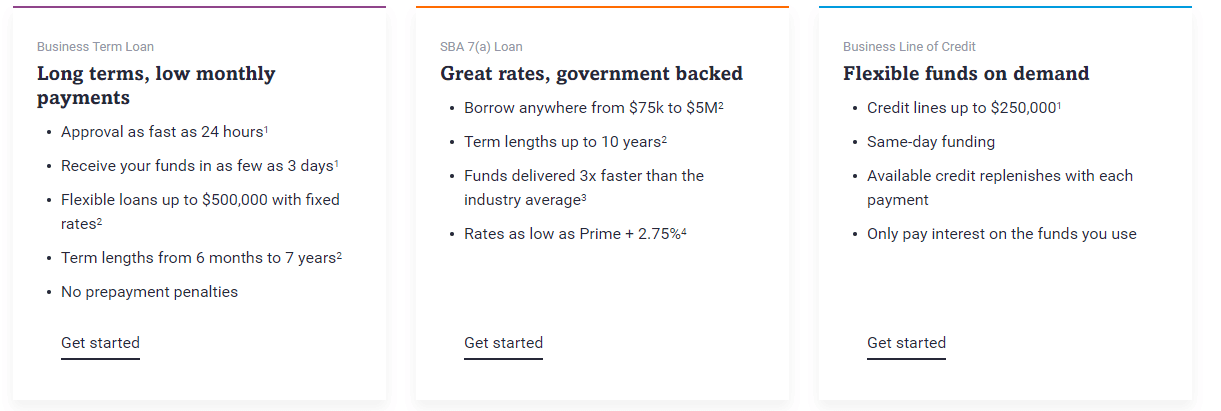

Get a business term loan for a term of six months to seven years. Get funding in as little as three days. Enjoy a loan of up to $500,000 with a fixed rate.

Get an SBA 7(a) loan for $75,000 to $5 million with a term length of up to ten years. The rates start at just the Prime + 2.75%. Receive funds three times as fast as the industry average.

Get a business line of credit for up to $250,000 with same-day funding. You only pay interest on the funds used. The credit replenishes when you pay.

There is no minimum revenue requirement, but you must be in business for at least two years. You can’t have had a bankruptcy in the last seven years.

You will need a personal guarantee and business lien.

Pricing

The typical APR is between 10.64% and 31.85%. For SBA 7(a) loans, the rates start at just the Prime + 2.75%.

There are no prepayment penalties for the loans from Funding Circle.

Bottom Line

Funding Circle will appeal to businesses that don’t meet the minimum revenue requirements of other loans, as there are no such requirements. However, the two-year minimum time in business required is longer than others on the list. Small businesses that need multiple types of loans or aren’t sure what works best for them will appreciate the ability to apply for a term loan, SBA loan, and line of credit all at once.

American Express acquired Kabbage, so you will sometimes see it referred to as American Express Small Business Loans and sometimes as Kabbage. This lender is an appealing choice for businesses that want fast access to funding and have a credit score of at least 640.

Highlights

Minimal documentation is needed to apply, and the application process is quick. You will need online checking to confirm your business cash flow.

You only need to have been in business for a year and have a minimum cash flow of $3,000 a month. At $36,000 per year, this is much less than other lenders.

The minimum credit score is 640.

You can receive up to $250,000 in funding within just a few days. Loans start at just $2,000.

You can choose from multiple types of loans, including unsecured and secured, as well as industry-specific loans. There are also loans for women and veterans.

Choose from a business line of credit or a short-term business, inventory, commercial, professional, working capital, SBA, equipment, or online loan.

The business line of credit can be for $2,000 to $250,000.

You make monthly repayments, while some lenders on this list require weekly or even daily repayments. That makes it easier to budget repayments.

There are no penalties for prepayment, nor are there fees for account maintenance.

Kabbage has shorter loan repayment terms, with your choice of six, 12, or 18 months. This makes it better for short-term loans.

Pricing

The pricing for your small business loan from Kabbage (American Express) will vary. On its website, it says that the average APR for small business loans is 3% to 60% APR. The average for a business line of credit is 8% to 80% APR.

The business line of credit from Kabbage comes with total monthly fees of 2% to 9% for six-month loans. The fee is 4.5% to 18% for 12-month loans. It is 6.75% to 27% for 18-month loans. You pay the loan fee every month there is an outstanding balance.

Bottom Line

Small businesses who want shorter-term loans or lines of credit should consider Kabbage. It is easier to qualify for a loan from Kabbage than from others on the list, as your business needs only $3,000 of monthly revenue and a year in business. You also get the confidence that comes from the reputation of American Express and your choice of type of loan. The industry-specific loans are useful if you want a loan tailored to your industry. Veterans and women who own businesses will find the minority loans, especially appealing due to their competitive terms.

Biz2Credit is much easier to qualify for than other loans on this list. You need a credit score of only 575 and be in business for at least six months. The lender also offers multiple types of loans, including CRE (commercial real estate) loans, term loans, and working capital.

Highlights

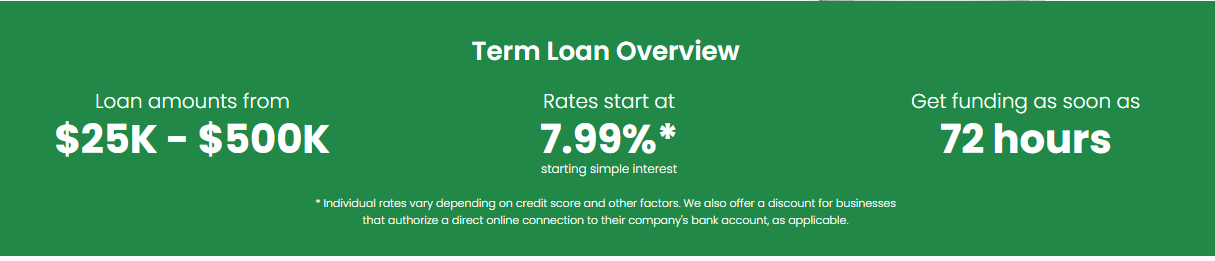

Term loans available for $25,000 to $500,000. Working capital loans are available for $25,000 to over $2 million. CRE loans are available for $250,000 to $6 million.

Get funding as soon as 72, 24, or 48 hours for term, working capital, and CRE loans, respectively. The application process takes about four minutes.

Term loans are popular for larger projects, offering stability. You can choose a term of 12 to 36 months. You can opt for weekly or biweekly payments.

Most businesses with term loans have a credit score of 660, at least 18 months in business, and annual revenue over $250,000. You can apply with lower figures.

Working capital loans are great for business expenses and projects. You repay from your business receipts. Choose daily, weekly, or biweekly payments.

Most businesses with working capital loans have a credit score of at least 575, six months in business, and annual revenue over $250,000.

CRE loans are ideal for major acquisitions or projects. Terms are 12 to 36 months. Take advantage of interest-only and monthly payment options.

A dedicated funding specialist will help you decide what type of loan is right for your business.

Most businesses with CRE loans meet the same requirements as those for term loans but already have commercial property.

Biz2Credit has funded more than 200,000 businesses. It has a 4.6/5 rating on Trustpilot.

Pricing

Opting for a term loan gives you simple interest rates starting at 7.99%. Commercial real estate loans have rates starting from 10%.

Bottom Line

Companies with shorter business histories or business owners with lower credit scores may want to consider Biz2Credit, especially its working capital loans. The company offers multiple loan types and has funding specialists that help you decide what makes the most sense for your business. Most loans are funded quickly, with many decisions occurring within 24 hours and businesses receiving funding in 72 hours.

Businesses in search of a line of credit instead of a traditional loan may want to consider Bluevine. As a line of credit, you get access to working capital very quickly. The lines of credit can be up to $250,000, and you need a minimum credit score of 625. Conveniently, you need to have been in business for only six months to apply, making this loan more accessible than some others.

Highlights

You can receive your funds within 12 to 24 hours and a decision as quickly as five minutes.

Applying is easy, requiring only basic details, bank statements or a bank connection, and good standing for your business.

Get a line of credit of up to $250,000. Draw funds as you need them, only paying for what you use. The credit line replenishes when you make payments.

Businesses need to be only six months or older, and your credit score just has to be 625. You also need $10,000 of monthly revenue.

Bluevine has an A+ rating from the Better Business Bureau. The line of credit comes from Celtic Bank, which is an FDIC member.

Bluevine also offers business checking, letting you handle all your business’s financial needs in one spot.

Pricing

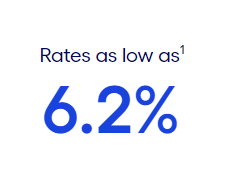

The rates for a business line of credit from Bluevine start at just 6.2%. That said, rates can go up to 78%.

Bottom Line

Compared to some other lenders, Bluevine has minimal requirements, as your business just needs to be at least six months old, and your credit score just has to be 625. Bluevine’s line of credit is easy to use, making it highly appealing. You can easily manage everything via the app or online, including requesting funds, making payments, and viewing your available line of credit.

With National Funding, you can choose from several types of loans. Small business loans include unsecured loans, working capital loans, and business loans for women. The company also offers equipment leasing, which can be useful if your company needs additional equipment.

Highlights

Get a small business loan of $5,000 to $500,000 or finance or lease equipment up to $150,000.

National Funding has provided more than 75,000 businesses with more than $4.5 billion.

It has a 4.8/5 rating on Trustpilot with more than 1,500 reviews and an A+ BBB rating.

You can receive a decision and your funding in just 24 hours.

A funding specialist helps you determine what type of loan makes the most sense for your business.

Short-term loans are available for six to 18 months. Unsecured loans are available with competitively low requirements.

Women, minorities, and veterans will find it easier to get a loan from National Funding via its special programs.

Loans are available for those with bad credit. Short-term loans can help you improve your credit score. A minimum score of 600 is recommended.

Equipment financing comes with a Lowest Payment Guarantee and no need to make a down payment. It requires a FICO score of 575 and six months in business.

Early payoff discounts are available, with a discount of 6% or 7% depending on when you pay off the loan.

Pricing

The rates from National Funding start at 4.99%. Importantly, your rate will depend on numerous factors. You can get an estimate of your rates and the size of the loan you qualify for by filling out a simple form on the National Funding website, including selecting your annual gross income.

Bottom Line

Small and medium businesses will want to consider National Funding for its short-term loans, working capital loans, and equipment financing options. The lender’s requirements are not as strict as others in the industry. It also offers early payoff discounts in some cases. The caveat is that you need gross annual sales of at least $250,000, which may mean some smaller businesses are not eligible.

Kiva is a unique option for small business loans, as it is a non-profit that hopes to expand financial access to communities that are underserved. The loans from Kiva are crowdsourced, meaning the organization lets people in good financial positions help those who are struggling.

Highlights

Get a loan for up to $15,000 with 0% interest. You will not find a better interest rate than that. You also get free marketing to appeal to the lenders on Kiva.

4.5 million borrowers in 79 countries have received loans of $1.82 billion through Kiva. These loans come from 2.1 million lenders with a 96.4% repayment rate.

You can fill out the Kiva application in just 20 to 30 minutes after confirming you are pre-qualified. You have up to 15 days to invite family and friends to lend to you.

You have up to 30 days to fundraise on Kiva, where 1.6 million lenders worldwide may see your loan request. You have up to 36 months to repay the loan.

To qualify for the loan, you must reside in the United States, be at least 18 years old, and use the loan for business.

You will need to have a few family and friends loan you money. You also can’t be in bankruptcy or foreclosure or have liens. Lenders can lend as little as $25.

Pricing

Impressively, the loans from Kiva of up to $15,000 have 0% interest. This comes from the fact that it is a non-profit organization looking to expand access to capital.

Bottom Line

If you don’t want to turn to traditional loans, Kiva is worth consideration. What makes it unique is that it is a non-profit organization that connects lenders and borrowers for crowdfunding. You can borrow up to $15,000 with Kiva, and best of all, there is no interest to pay. You will, however, have to make your loan request seem appealing to encourage lenders to fund you.

What Are Small Business Loans?

Small business loans are a way for small business owners to get funding. Business owners can use these to cover the costs of regular operations or growth. There are numerous loan options, including many from banks, as well as those from the U.S. Small Business Administration (SBA). Many loans don’t restrict how you use the funds as long as it is related to your business, but some will restrict it to certain uses.

Our list of the best small business loans includes options for everyone. You will notice that they allow you to borrow various amounts, and some give you access to the funds faster than others.

Types Of Small Business Loans

In the above list, we mention several different types of small business loans. It’s important that you understand the differences between these, so you know what type of loan to apply for.

SBA Loans: SBA (Small Business Administration) loans are guaranteed by the SBA. They tend to have longer repayment terms and lower interest rates. But they also have more demanding requirements. There are several types, including the next few items on this list.

SBA 7(a) Loans: These can be up to $5 million and are the most common SBA loan. These types of loans can be used to buy real estate or business supplies, get working capital, or refinance debt.

SBA 504 Loans: These can be up to $5 million and have to go to major fixed assets. Examples include long-term equipment and machinery, new facilities, existing buildings, or land. You cannot use them for inventory, working capital, or other uses.

SBA Microloans: These are up to $50,000. They are specifically for small businesses getting started or looking to grow. The funds can be used for business supplies, equipment, machinery, inventory, working capital, and more.

Term Loans: These are traditional loans that your business repays over time. You receive a lump sum and pay interest on the full amount. Short-term loans may last three to 18 months or so. Long-term loans can last ten years or even longer. These are typically versatile, but some may limit how you use the funds.

Lines of Credit: A line of credit gives you revolving access to funds. As you pay off the balance you owe, you can borrow more money. Lines of credit typically last for shorter periods of time, such as five years or so. After the draw period is done, you enter the repayment period. At this point, you have to pay back any remaining balance. Importantly, you only pay interest on the portion of the line of credit that you use.

Equipment Financing: This loan specifically helps you access equipment your business needs to function. It can be used for nearly anything, including manufacturing equipment, electronics, and office furniture. You can find options with terms of up to 25 years and loans of up to $1 million or even more. Interest rates are usually 8% to 30%.

In addition to the above, there are a few other types of business loans you should be aware of. We didn’t include any of them above, but some of the lenders mentioned do offer them. Even if you stick to our list, being aware of these types of small business loans will enable you to know all your options and decide on the right one for you.

Invoice Factoring: This involves selling outstanding invoices from the business for a lump sum cash payment. The third-party factoring company buys the invoices at a discount. They then become responsible for collections. This can get you up to $5 million with an APR of 10% to 79%.

Merchant Cash Advances: These are typically funded by merchant services companies and involve businesses receiving a portion of their future sales receipts. The repayments come directly from the individual sales or through ACH weekly or daily. Repayment is in a set percentage of daily credit card sales.

How To Use Our Recommendations

When you are ready to get a loan for your small business, use the above information to confirm the type of loan you need. You can also use all these options to determine how much you need to borrow and your loan term preference.

Consider how your business stacks up in terms of common requirements. Make sure you know your personal credit score, your time in business, and your average annual business income.

Then, choose one of the lenders from our list that fits your requirements. Confirm the documents they need. Expect to be required to provide documentation like bank statements or tax returns. You will also likely need legal documents and your business license.

Once you have all these, you can apply. All the small business loans on our list have online applications that you can complete fairly quickly.

Conclusion

With the above options, it should be easy to find the best small business loans for your company. As you decide, consider the various types of loans and your credit score. Don’t forget to strategize how you plan to use the funds and how much you need to borrow as well. The bottom line is that you can apply for any of the business loans on our list with confidence.

Shawn Manaher

Shawn Manaher is a former financial advisor, has founded 5 online businesses, and is a coach, speaker, podcast host, and author.

He's been featured on Forbes, The Consults Corner on TAE Radio, The Writing Biz, What's Your Story, and more.

He loves to share his personal finance tips and money management wisdom with others to help them find financial freedom.