5 Best Credit Cards for Bad Credit for December 2023

Shawn Manaher

•

Updated on November 11, 2022

When you have bad credit, it can be incredibly challenging to find a credit card or be approved for a loan. While it may be harder, it is still possible to get a credit card. Even better, using the card responsibly will help you build your credit score, making your financial future easier. We’ve gathered the best credit cards for bad credit, so you know which ones to consider applying for. Any of the cards on our list would be a great choice; you just have to decide which one best fits your needs.

Table of Contents

What Are the Best Credit Cards for Bad Credit?

Before you can apply for a credit card online with bad credit, you will want to narrow down your options. There are dozens of cards, but many credit card offers for bad credit will take advantage of your financial situation. You may pay high fees with no benefits for you.

To avoid issues, keep the following considerations in mind as you look into how to apply for a credit card with bad credit.

Secured vs. unsecured: The very first thing to consider is whether you want secured or unsecured cards. Unsecured or traditional cards don’t require an initial deposit. Secured cards require a deposit that becomes your spending limit. It is much easier to get a secured card if you have bad credit than an unsecured one. But your spending limit will be limited by how much you can afford to deposit. That can tie up your funds until your deposit is refunded.

Whether a credit check is required: Traditional cards typically require a credit check, which is hard to pass if you have bad credit. But many cards for bad credit do not require a check. If your credit score is bad but you have otherwise good financials, you may want to choose a card that considers other factors instead of or in addition to checking your credit.

If you can be pre-approved: Some of the cards on our list offer pre-approval without affecting your credit score. This is important because applying will usually affect your credit score. You can check if you are pre-approved and then only apply if you are likely to qualify.

Reporting to credit bureaus: If your credit is bad, you can use your new credit card to rebuild your score. But this will only work if your card issuer reports to credit bureaus. So, be sure to choose a credit card that reports your on-time payments and credit utilization to the bureaus. Ideally, the card will report to all three major bureaus, but reporting to one or two is better than nothing.

Annual fees: Companies see offering a card to someone with bad credit as a risk, so annual fees may be high. But you can easily find several options with low or no annual fees. Always opt for a card without an annual fee unless it offers something unique that makes the fee worth it. For example, the one unsecured card on our list has an annual fee, which is justified by the fact that it is unsecured.

Hidden fees: Many unscrupulous card issuers prey on people with bad credit and their desperation. They may hide additional fees, such as “issuance fees,” in the fine print. It is important to read all of the fees before applying for a card. Reviews can also help you spot hidden fees.

APR: You also want to pay attention to the APR or interest rate for the card. You will hopefully pay your balance in full every month, but opting for a card with a lower APR protects you in case you can’t do so. Unfortunately, part of getting a credit card with bad credit includes putting up with high APRs.

Limits: Expect the credit limit on your credit card for bad credit to be lower than it would be for someone with a better score. That being said, several cards offer limits of up to several thousand dollars, and a few even go up to $10,000 or more. Having a higher limit makes it easier to keep your credit utilization ratio low, boosting your credit score. However, don’t opt for a high limit if you don’t trust yourself to only spend what you can pay off. Otherwise, you will dig yourself into a financial hole with the high interest rates.

Security deposits: As most of the credit cards for those with bad credit are secured cards, you can expect to have to make a security deposit. Pay attention to the size of the deposit as well as how long you have to make it after approval. Your deposit will typically become your credit limit, and there are two sides to this consideration. If you don’t want to tie up a lot of your cash in a refundable deposit, look for a card with a low deposit, such as $100 or $200. If you have the cash to spare and want a higher limit, consider one of the cards that let you deposit up to $1,000 or $2,000 to get the limit you want.

Path to upgrade and deposit refund schedule: Some secured credit cards won’t refund your deposit until you close your account. The best ones, however, will refund it after a certain number of on-time payments or an improvement to your credit score. When your deposit is refunded, your secured card becomes an unsecured one. In other words, you get a simple upgrade path. The Capital One Platinum Secured Card, for example, can be upgraded to the Capital One Platinum (Unsecured) Card. The Discover It Secured Credit Card also offers a simple upgrade path.

Other cards from the issuer: You tend to have more options for an upgrade path if your secured card comes from a card issuer with multiple options. After all, both Discover and Capital One are major names. Simply put, if an issuer offers a wider variety of cards, the process of switching in the future should be easier, and you may be approved for a higher limit because of your history with them.

Rewards: Only a handful of bad-credit credit cards offer rewards, but options do exist. In most cases, choosing a card with rewards will have a trade-off of some sort, such as an annual fee. So, always compare the benefits of the rewards to the other drawbacks of the card.

Balance transfers: Few bad-credit credit cards offer special rates for balance transfers, but some do. If you want to transfer a balance, consider one with an introductory balance transfer APR. This is unlikely to be zero, but it may be significantly lower than the normal APR.

Credit score tracking and education: The best credit cards make it easy to track your credit score. Some of the options on our list let you do so easily via their mobile apps or your online account. This feature helps you follow improvements to your score to confirm you are on the right track.

With those considerations in mind, take a look at the best credit card offers for poor credit. These best credit cards for bad credit include both secured and unsecured options and a range of annual fees.

The OpenSky Secured Visa is a secured credit card that helps you build your credit score with responsible use. It provides all of the benefits of a Visa card. OpenSky also offers plenty of educational resources and tips to help you build your credit score. Additionally, it’s easy to apply, and you don’t have to pass a credit check to do so.

Highlights

No credit check is required, so applying doesn’t affect your credit score. The application takes five minutes.

OpenSky reports to all three major credit bureaus every single month. This maximizes the positive impact the card has on your score.

You choose how large of a refundable (FDIC-insured) deposit to make, between $200 and $3,000. This becomes your credit limit.

You may be eligible for a credit increase without an additional deposit after six months. You may also qualify for an OpenSky Gold Unsecured Card at this point.

Set up email alerts to avoid missed payments or set up automatic payments. Email alerts can also tell you if you are getting close to your credit limit.

99% of cardholders without a credit score build their score within just six months.

Enjoy all the Visa benefits, including the ability to use it anywhere internationally and fraud protection.

OpenSky offers advice for building your credit, including a dedicated “Resources” section of its website.

In the last five years, the approval rate has been about 85%. You will be approved (or rejected) instantly.

View your FICO score for free via your account.

Pricing

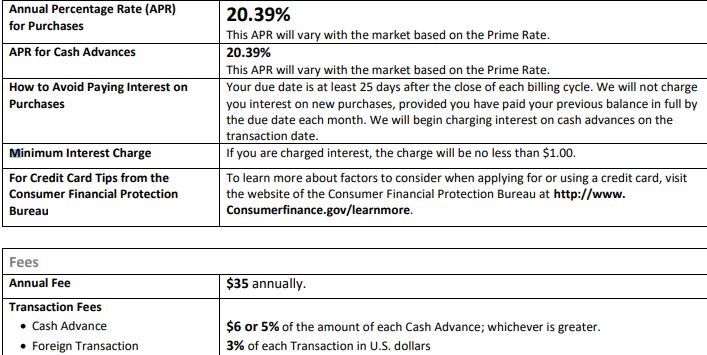

The annual fee for this card is just $35. This is among the lowest annual fees for cards that charge one.

The interest rate is 20.39% APR. The minimum interest is $1.00 if you are charged any interest at all.

There are no application fees or fees for servicing or processing. The cash advance fee is $6 or 5%, whichever is greater. Foreign transaction fees cost 3% of the transaction. Late payments have a fee of up to $38, while returned payments cost up to $25.

Bottom Line

The OpenSky Secured Visa is a strong choice if you have a bad credit score or no credit history, as there is no credit check required. It can appeal to people without any bank accounts, as you can choose from several methods of making your initial deposit and monthly payments. This secured card is designed to help you build your score with on-time payments, thanks to reporting to all three bureaus. It also offers one of the largest ranges for potential deposits and, therefore, credit limits among secured cards, helping it appeal to those who want very small deposits or higher limits. Importantly, OpenSky also approves people who owe back taxes and have bankruptcies, something which is rare even among cards for people with bad credit.

Those who want a secured card with rewards and no annual fee should consider the Discover It Secured Credit Card. This is one of the few options that lets you sign up for a credit card with bad credit and earn rewards. It is also one of the few options for bad credit with a balance transfer promotional APR.

Highlights

You can check for pre-approval without hurting your credit score, so you know whether to apply.

You can apply without a credit score as long as you meet other requirements. Discover may consider your credit score if you have one.

Choose a security deposit between $200 and $2,500, which becomes your credit limit. The maximum limit is based on your ability to pay and your income.

Your deposit can be refunded after six months of on-time payments if all other credit accounts also have a “good status.” Reviews begin after seven months.

Discover reports to all three credit bureaus, helping you build your credit score with on-time payments and low credit utilization.

Earn 2% cash back at restaurants and gas stations (up to $1,000 per quarter). Earn 1% cash back on all other purchases.

Discover matches your cashback rewards earned in the first 365 days or 12 consecutive billing payments of having your card.

View your FICO Score for free, making it easy to track it.

Use the Discover app to activate online privacy protection. Regularly have your information removed from 10 people-search websites that may sell your data.

Activate free alerts for your social security number. Never pay for unauthorized purchases.

Pricing

The Discover It Secured Credit Card has an APR of 25.99% that varies based on the Prime Rate. This 25.99% APR also applies to balance transfers after the first six months. For the first six months, balance transfers have an introductory APR of just 10.99%. The APR for cash advances is 27.99%. Any time you are charged interest, it will be at least $0.50.

There is no annual fee. In addition to the APR, cash advances have a fee of 5% or $10, whichever is larger. Returned payment fees are up to $41. Late payments are up to $41, but you don’t pay a fee for the first late payment.

Bottom Line

The Discover It Secured Credit Card is a good option for those with bad credit who want to earn rewards and have no annual fee. It is one of the few options if you want to get approved for a credit card with bad credit and earn rewards for using your card. This card also makes it easy to upgrade to an unsecured card because it is from a major card issuer. Just keep in mind that you must make the initial deposit with a bank account. If you are currently unbanked, this may be a challenge.

As the name implies, the Credit One Bank Platinum Visa for Rebuilding Credit is specifically designed to rebuild your credit score. It offers the ability to earn rewards, but there is an annual fee. Importantly, this is one of the rare unsecured options if you want to get approved for a credit card with bad credit. This makes it highly appealing if you don’t want to tie funds up in a deposit or can’t afford a deposit.

Highlights

Earn 1% cash back on eligible purchases, including groceries, gas, and monthly bills for phone, cable, internet, satellite TV, and more.

Earn up to 10% more cash back rewards from certain retailers.

Credit One Bank regularly reviews your account to see if you are eligible for a credit line increase.

Access the mobile application, which is easy to use. Use the app to access your credit score for free, change your payment due date, and customize notifications.

Set up notifications for payments due, payment confirmation, and posted activity. Opt for text or email notifications.

Customize your card with a premium design, or get a second card for an authorized user for a fee.

Connect your credit card to Google Pay, Samsung Pay, and Apple Pay.

Monitor your credit score over time to see changes, including a monthly summary of your credit report.

You have zero fraud liability.

Your credit line is at least $300 and may increase over time.

Pricing

The annual fee for the first year is $75. After that, it is $99, billed monthly at $8.25 a month. The APR is 26.99% variable. When you owe interest, it will be at least $1.

Cash advance fees are $5 or 8%, whichever is larger. Foreign transaction fees are 3% or $1, whichever is larger. Late payment fees are up to $39. Returned payment fees can also be up to $39.

The fee to add an authorized user with their own card is $19.

Bottom Line

For those who want to know “what credit card can I get with bad credit?” and don’t want a secured card, this Credit One Bank card is an excellent option. It is one of the few unsecured cards for bad credit, and you also get to earn rewards for your purchases. The only downside is that there is an annual fee, but that’s to be expected from an unsecured card for bad credit.

The Capital One Platinum Secured Credit Card is an excellent option for a secured credit card for bad credit without an annual fee. Additionally, you may be able to apply for a credit card bad credit limit that is higher than your initial deposit. You can also check if you are pre-approved without affecting your credit score. This card also has a clear path to upgrade to an unsecured card, making it appealing if that is your ultimate goal.

Highlights

Check for pre-approval without affecting your credit score.

Get an initial limit of $200 by depositing $49, $99, or $200. Depositing more can earn you a limit of up to $1,000 initially.

Responsible use can mean you upgrade to an unsecured Platinum card and have your deposit refunded. You may also get a higher limit without an additional deposit.

You may be considered for a credit line increase within six months.

Capital One reports to all three major bureaus, helping you quickly build your credit score and history.

Set up account alerts and auto pay to help you with your money management.

Add an authorized user and track their spending.

Use the mobile app to view transactions and balances, use CreditWise, pay your bill, and more.

Keep your money safe with $0 fraud liability, security alerts, card lock, account alerts from Eno, and virtual card numbers from Eno.

CreditWise alerts you about changes to your credit report from TransUnion or Experian. It also lets you view your credit score.

Pricing

This Capital One Secured Credit Card has an APR of 28.49%. There is no annual fee.

Balance transfer fees are 3%. Cash advance fees are 3% or $10, whichever is larger. Late payment fees are up to $40.

The deposit is refundable and a minimum of $49, $99, or $200, depending on your financial situation. There are no hidden fees, including for foreign transactions, authorized users, or replacement cards.

Bottom Line

The Capital One Platinum Secured Card is a solid choice for those who want to be able to easily upgrade to an unsecured credit card. Given that it has no annual fee and reports to the major credit bureaus, this card is also a useful tool for building your credit score. It is also one of the few secured credit cards that can give you a limit that is higher than your deposit, making it appealing to those on a tight budget. The only caveat is that, depending on your credit history, you may not be approved, especially if you have a bankruptcy. You also need a savings or checking account to qualify.

The Tomo Credit Card is a secured credit card with a unique approach, as you cannot carry a balance. This makes it a good way to get into good spending habits, including only spending what you can pay off. It also means that you don’t have to worry about interest rates. The card is a particularly solid option for immigrants, as it considers factors other than your credit score, and you don’t need to be a U.S. citizen to be approved.

Highlights

Enjoy up to $10,000 of spending power. Minimum spending power is $100. Increase spending power with on-time payments and by linking more bank accounts.

No credit history is needed. Instead, Tomo looks at other factors, such as your bank accounts. Applying doesn’t affect your credit score.

Anyone can apply with a government-issued ID and SSN or ITN. You don’t have to be a U.S. citizen.

Tomo reports to all three credit bureaus. Pay your balance weekly for faster improvements to your credit score.

Earn $5 credit when you take three rides with Lyft, a $60 value. You can also get three months of DashPass and then $5 off for the following months, a $90 value.

Receive discounts on your first five HelloFresh boxes plus free shipping, a $90 value. Get a free ShopRunner membership plus free shipping and returns, a $79 value.

As a World Elite Mastercard, get $5 off a purchase on Fandango when you spend $20. Access travel rewards in 40 cities, a 24/7 World Elite Concierge, and PGA Tour experiences.

Get $1,000 cell phone protection if your phone is damaged or stolen.

Enjoy MasterCard ID Theft 24/7/367, global emergency assistance, and zero liability for unauthorized purchases.

Because there is no APR, you cannot carry a balance. If you don’t pay off your balance, the card is frozen until you do.

Bottom Line

The Tomo card is a solid option if you want to get a credit card with bad credit or no credit. It especially appeals to immigrants, as you just need an ID and an ITN or SSN. The card is appealing to anyone looking to avoid fees and accidentally carrying a balance, as it is impossible to do so. At the same time, the ability to set up automatic payments every week helps you rebuild your credit score even more quickly than you will with other options.

How To Apply For A Credit Card With Bad Credit?

The process of how to apply for a credit card with bad credit is the same as it would be to apply for any other card. The biggest difference is that you will want to apply for one of the best credit cards for bad credit on our list, not just any card. Applying for a credit card you are unlikely to be approved for will hurt your score needlessly.

Step 1: Assess Your Credit Score

Before you look into how to get a credit card with bad credit, confirm that you know what your score is. Perhaps your score is not as bad as you think, and you can apply for a card with average credit.

Even if your score is “bad,” knowing what it is will be important. This will let you track improvements to it as you pay your credit card bills on time and keep your utilization ratio low.

This is also the time to look at your credit history. If, for example, you have a bankruptcy, it will be best to apply for a card that specifically accepts people with bankruptcies. General bad-credit credit cards may still not approve you.

Step 2: Assess Your Needs and Preferences

Next, think about how you plan to use the credit card and whether you have any preferences. This is where the considerations mentioned above come into play. The first preference to consider will be if you are okay with a secured card or prefer an unsecured one. As you can tell from our top picks for credit cards, it is much easier to get a secured one, but there are some options for unsecured cards.

This is also the time to weigh the pros and cons of rewards versus fees. When building credit, it is typically best to avoid annual fees and high APRs if you can, even if that means sacrificing potential rewards.

Step 3: Choose A Card

With your preferences in mind, it’s time to choose which card to apply for. The easiest option is to choose one of our recommendations listed above. This will save you the hassle of having to research various cards and confirm that they accept people with bad credit. Remember that some card issuers define a bad credit score as anything below 630. Others consider anything under 580 to be bad.

Step 4: Get Pre-Approval (If Applicable)

You will notice that some of the cards on our list let you get pre-approved without affecting your credit score. If this is an option on your chosen card, take advantage of it. This will let you confirm your approval before you actually apply. That is important as applying will frequently involve a hard inquiry which can temporarily hurt your credit score. Applying to too many cards in a short time will hurt your credit score and make it harder to be approved for a card or loan.

By getting pre-approval, you limit the impact on your credit score. After all, your goal is to use your new credit card to build credit, not to hurt your score while applying.

Step 5: Apply

You are finally ready to apply for your chosen credit card. Most cards let you apply online in a matter of minutes. Depending on the card, you may also be able to apply over the phone, by mail, or in person at a physical location.

To apply, expect to provide the following at a minimum:

Your name

Your birthdate

Your address

Your social security number

Your income

Depending on the card you are applying for, you may also be asked for other information. Some, for example, ask for information about your bank accounts. This is especially common with cards that don’t require a credit check.

Step 6: Make A Deposit (If Applicable)

If you get an unsecured card, you will likely be ready to use your card. If you have a secured one, you will need to make a deposit before you can start using it. Remember that your deposit will affect your credit limit.

You should have the funds for your deposit on hand before applying for the card. That is because most cards require you to make the deposit within a few days of approval. Not depositing in time can cause the card issuer to rescind your application.

Step 7: Use Your Card Responsibly To Build Credit

Now that you have your card, it is time to use it responsibly to rebuild your credit score. Keep the following in mind:

Pay on time: On-time payments account for 35% of your FICO credit score. At a minimum, make your card’s minimum payment. Ideally, you want to pay your balance in full every month. This prevents you from accumulating interest, which can make it harder to pay off your balance. It also helps you keep your credit utilization ratio low.

Keep your credit utilization ratio low: Speaking of your credit utilization ratio, try to keep it below 30%. This accounts for 30% of your FICO score. This means that you should try not to use your full credit limit. For example, if your line of credit is $200, you want to keep your balance under $60 (30% of $200).

Keep old accounts open (if there’s no annual fee): Your credit history length affects 15% of your credit score. This means that it is good to keep old accounts open unless they charge an annual fee. For most people, it is not worth paying an annual fee on a card you don’t use just to boost your credit score slightly.

Wait to apply for another line of credit: Once you get your credit card, wait for a little while to apply for another credit card or loan. Applying for too much credit in a short period of time can make you seem desperate.

Remember that your credit score doesn’t just affect your ability to get a credit card or loan. It can also affect whether you are hired for a job, approved to rent a property, or even if your utility company or cell phone provider will work with you.

Conclusion

The best credit cards for bad credit tend to be secured cards. These will have the highest approval rating. Before you apply credit card bad credit, compare annual fees and potential rewards from various cards. You should always choose a card that reports to the credit bureaus, as this will help you improve your score and get a better card in the future.

Shawn Manaher

Shawn Manaher is a former financial advisor, has founded 5 online businesses, and is a coach, speaker, podcast host, and author.

He's been featured on Forbes, The Consults Corner on TAE Radio, The Writing Biz, What's Your Story, and more.

He loves to share his personal finance tips and money management wisdom with others to help them find financial freedom.